The World Bank has recently performed some tests researching the uses of central bank digital currencies and digital money, and their uses in wholesale and retail settings.

Wholesale CBDC is predominantly used by central banks and financial institutions for interbank lending and transfers. Retail CBDC is stored in digital wallets and used by consumers for the purchase of goods and services.

Published on July 2nd, The World Bank released its document called “Interoperability Between Central Bank Digital Currency Systems and Fast Payment Systems: A Technical Perspective.” The abstract of the piece explains the purpose of their research:

Central banks around the world are actively researching and investigating the benefits, challenges, and design options of wholesale and retail central bank digital currencies (CBDCs). Since CBDCs are one of the most critical components of a national payment system (NPS), it is important that their interoperability with other payment systems is one of the key considerations in the design process. The ITS Technology and Innovation (ITSI) team, in collaboration with the World Banks’s Finance Competitiveness and Innovation (FCI) Global Practice, has conducted technology design experiments on two specific scenarios regarding CBDC system interoperability with fast payment systems (FPS).

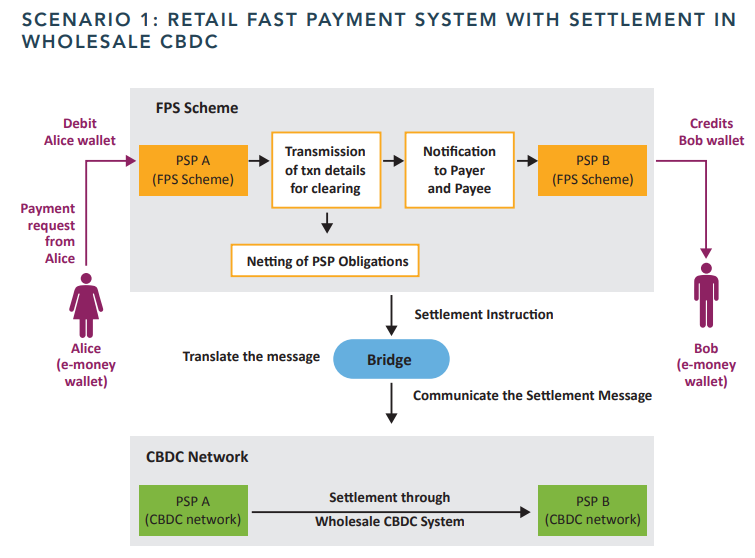

In the first scenario, the experiment investigated the option of settling FPS obligations in a wholesale CBDC system, including the option to reserve funds to guarantee the settlement of FPS net obligations.

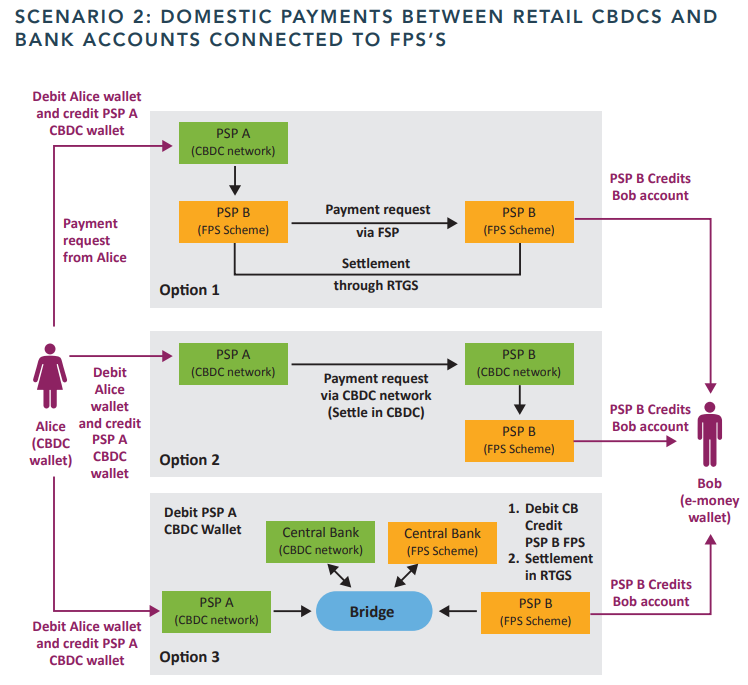

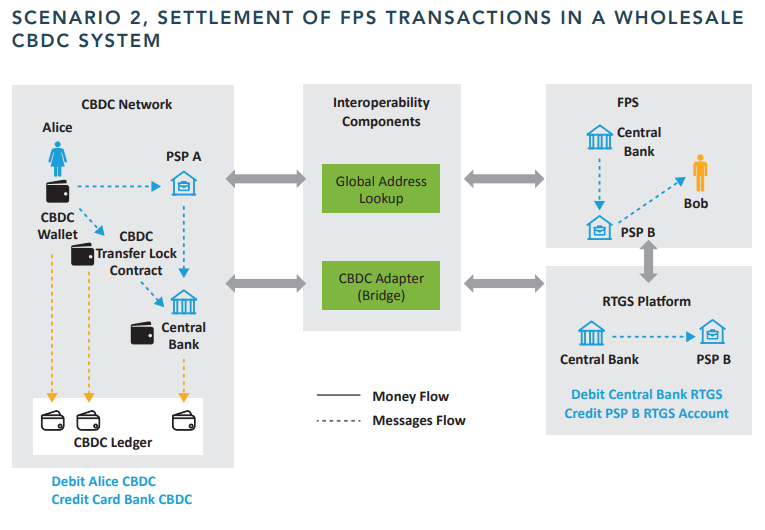

In the second scenario, the team investigated the interoperability between users within the FPS and retail CBDC users, including the transfer of funds among both types of users, using common services such as address resolution services. This experiment illustrated how CBDC systems can interoperate with retail payment systems through an interlinking bridge that was used to route messages and application programming interface (API) calls among different systems. The programmability features of distributed ledge technology (DLT) were used to link the settlement in CBDC to the transfer of funds in the FPS.

The technical applicability for this type of interoperability was demonstrated through the experiments, with the caveat that these experiments do not take into account complexities that may be involved with live systems.

The paper follows this opening statement by explaining the necessity for interoperability and the use of CBDCs via instant-transfer payment rails. The authors wrote:

The interoperability between CBDC systems and other payment systems is essential in

order to avoid fragmentation in the national payment system. For the CBDC to be used in any jurisdictions at all it should have the rails to be exchanged with existing payment instruments; otherwise it would have limited practical value.

Interoperability allows the CBDC to enhance overall payment system efficiency within the jurisdiction, because the CBDC can provide instant settlement and extended access to excluded segments of the community, or even to nontraditional payment service providers (PSPs). CBDC interoperability allows a seamless flow of value across various forms of money and different types of accounts.

Domestic payment system interoperability with other domestic payment infrastructures is a key challenge in CBDC design. CBDC interoperability with payment systems such as the Real Time Gross Settlement (RTGS) system or a fast/instant payment system–and the exchangeability with other forms of money such as e-money, commercial bank money, or cash– are essential for smooth end-to-end payment flow.

Even if the CBDC assumes the same value of unit of money in the jurisdiction, it would need to be booked in distinct systems at the central bank, or even by payment service providers; therefore CBDCs need to have special accounts, or stores of value, from other forms of money.

Last year, when the Federal Reserve debuted its 24x7x365, instant-transfer payment rail system FedNow, the Feds addressed criticisms that FedNow would be used as a launchpad for CBDCs; however, previous quotes from the Fed suggest otherwise, along with an official document published by the Biden White House that admitted FedNow would allow the central bank to leapfrog into CBDCs at some point.

The authors went on to answer their own question, “How can indirect participants in a wholesale CBDC system, such as nonbank e-money issuers, or payment service providers, settle their transactions in the (Fast-Payment System) FPS?”

The World Bank answered: “Possibly there could be a more sophisticated settlement structure in the CBDC system to allow direct participants in the FPS to settle their transactions indirectly in the CBDC system through a direct participant in the system such as a commercial bank. Such arrangements will need to identify limits for the indirect participants within the CBDC, defined by the direct participants in order to mitigate credit risk.”

In the instance of using a CBDC for retail, the World Bank listed the steps in its scenario as to how this would work:

Step 1: Participants in the FPS need to reserve funds in the Real Time Gross Settlement (RTGS) system, to guarantee the settlement of their net obligations in the FPS. These reserves are held in the RTGS system, and can be used only to settle FPS net results.

Step 2: The payer initiates the transaction through its payment service provider (PSP) from the payer’s rCBDC account, using the payee’s payment address alias.

Step 3: The payer PSP locates the payee PSP through the account look-up service in the

rCDBC system.

Step 4: The transaction fee is communicated to the payer, and the payer confirms the

transaction.

Step 5: The payer PSP identifies the payee as a non-rCBDC account, thus executes the transfer transaction to the payee’s PSP through the bridge that is managed by the central bank.

Step 6: The payer PSP pays the transfer value to the central bank in the rCBDC system,

usually? through the bridge component.

Step 7: The central bank initiates a transaction to the payee PSP within the FPS.

Step 8: The payee PSP transfers funds through the FPS to the payee.

Step 9: Notification is sent to both payer and payee by their respective PSPs.

Step 10: The central bank and the payee PSP obligations are recorded in the FPS for netting, and batched together in the settlement window.

Step 11: Settlement instruction is sent from the FPS to the RTGS so that the settlement from the central bank to the payee PSP will take place in central bank money from their prefunded accounts.

CBDCs, if and when they are introduced, will become a critical component not just in the context of national payment systems but may also have significant importance in the context of cross-border payment infrastructures.

The jury is still out with regard to what form and shape the CBDC systems will have; however, it is fair to state that CBDC interoperability with legacy and new payment systems will be essential in order to avoid furthering payment system fragmentation.

The World Bank concluded

AUTHOR COMMENTARY

Per usual, groups such as the World Bank pretend to be indifferent and play stupid, like using words and phrases such as “if” countries adopt CBDCs.

Back in April, I reported on the heads of the World Bank and Verizon who claimed that digital IDs are part of the “social contract” between government and citizens. World Bank Group President Ajay Banga made some incredibly dystopian statements regarding digital IDs, how “a sense of crisis is your best friend. Never let a crisis go waste,” he said; or other comments where he said, “I believe your government should be the owner of your digital ID,” and many other remarks like it. Total Orwellian, draconian statements being made right out in the open; so don’t fall for the mild speech used in this document they just put out.

CBDCs are a lock, and they are not that far away. A staged crisis will be needed to hedge their way in and be forced on a frightened mass of people around the world. Something like a massive cyberattack, IT outage, EMP, grid-down scenario I think is what might happen; draining bank accounts dry, let panic ensue for a little bit, then offer up the solution to a desperate, scared, hungry population…

Job 2:4 And Satan answered the LORD, and said, Skin for skin, yea, all that a man hath will he give for his life.

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

What a convoluted mess.

No matter how you slice transactions (now or in the future) it all goes back to the same criminals.