The U.S. Federal Reserve is claiming that their new digital instant transfer payment system FedNow is not designed to facilitate a central banker digital currency (CBDC).

In the wake of the banking tsunami scare and contagion after the collapse of Silicon Valley Bank on March 10th, on the 15th the Federal Reserve quietly announced that their instant payment system is set to launch this July. FedNow will operate at all times and will allow payments and transfers to be accomplished at rapid speeds, interlinked with larger banking institutions. Formal certification for banks interesting in joining this program began on the first of April.

The WinePress detailed its release last month: “Red Alert: Federal Reserve Set To Launch “FedNow” Digital Payment System To Usher In CBDC”

When the Federal Reserve made it’s March announcement some financial experts and analysts immediately said that this would ultimately lead to a new digital dollar and CBDC.

However, the Federal Reserve recently responded to this claim, unequivocally claiming that FedNow will usher in no such thing. On April 7th the Federal Reserve, answering their own question – “Is FedNow replacing cash? Is it a central bank digital currency?,” the Fed said no.”

They wrote:

No. FedNow is not related to a digital currency. FedNow is a payments service the Federal Reserve is making available for banks and credit unions to transfer funds. It is like other Federal Reserve payments services, such as Fedwire and FedACH. The FedNow Service is neither a form of currency nor a step toward eliminating any form of payment, including cash.

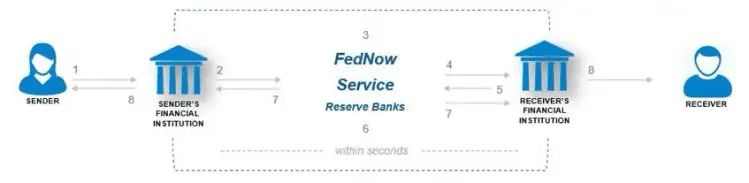

The FedNow Service is an instant payments service provided by the Federal Reserve, launching in July 2023. FedNow will be available to depository institutions, such as banks and credit unions, in the United States and will enable individuals and businesses to send instant payments through their depository institution accounts. Instant payments allow individuals and businesses to send and receive payments within seconds at any time of the day, on any day of the year, so that the receiver of a payment can use the funds almost instantly.

The Federal Reserve has made no decision on issuing a central bank digital currency (CBDC) and would not do so without clear support from Congress and the executive branch, ideally in the form of a specific authorizing law. A CBDC would not replace cash or other payment options.

The Fed stated

However, this statement conflicts with a previous statement the Fed made concerning FedNow last year. As noted in aforementioned The WinePress report about FedNow, Fed governor Michelle Bowman in a meeting last August, said that this system will essentially act as the launchpad for CBDCs as the Federal Reserve continues to develop theirs as do other central banks.

FedNow will help transform the way payments are made through new services that allow consumers and businesses to make payments conveniently, in real time, on any day, and with immediate availability of funds for receivers. Our assessment of these benefits has not changed even as we consider whether a central bank digital currency (CBDC) might fit into the future U.S. money and payments landscape.

My expectation is that FedNow addresses the issues that some have raised about the need for a CBDC. As I’m sure you are already aware, earlier this year we published a discussion paper that outlined some design principles, costs, and benefits of a CBDC and solicited public comments. We received over 2,000 comments, and we are currently reviewing these comments and plan to publish a summary of them.

She said during the VenCent Fintech Conference, Little Rock, Arkansas, last year

But some economists believe that FedNow is undoubtably designed to usher in a CBDC. Lena Petrova, a certified public accountant (CPA), explains that India has an identical system in place and that Indian officials have acknowledged that their instant transfer system is designed to usher in a CBDC of their own.

The more research you do on this, the more it becomes clear that the two systems go hand-in-hand and serve the same goal.

Petrova explained

Furthermore, even the White House and the Biden administration have acknowledged that both FedNow and a CBDC overseen by the Fed are indeed related, praising both for their speed and ease of accessibility, which has been further necessitated due to the shift in business and finances since 2020, the White House claims.

Released in March, the Biden Administration published an over 500-page document titled “The Economic Report of the President,” which discusses the prospect of FedNow and a CBDC. Chapter 8 deals with cryptos, and in a subsection titled “Investing in the Nation’s Digital Financial Infrastructure,” the White House acknowledges the introduction of FedNow and a CBDC.

Referencing the two, the White House admits that both systems are relatable:

This section first discusses an upcoming improvement to U.S. payments, which will help many consumers and businesses make cheap, instant payments. It then discusses the possibility of introducing a central bank digital currency (CBDC), which is a digital form of money. While operating under the supervision of a trusted authority, both these mechanisms have the potential to realize many of the benefits that crypto asset developers have promised.

The White House goes on to praise FedNow, claiming that it offers an “uninterrupted processing of fund transfers is an important improvement over existing payment systems.” Additionally the Biden administration wrote:

Beyond speed and convenience, near instant payments can yield real economic benefits for both individuals and businesses by allowing them to make time-sensitive payments whenever needed and providing them with more flexibility in managing their money.

In particular, near instant payments under FedNow could bring significant benefits to vulnerable segments of the population. Slow payment systems can cost Americans billions of dollars. In addition to incurring bank overdraft fees, consumers can be forced to use high-cost alternatives like check cashers and payday lenders.

In 2019, it was estimated that a fast payment system such as FedNow could reduce these kinds of fees, generating savings of more than $7 billion a year for American households. Because lower income individuals are more likely to be hurt by slow payment systems, they could especially gain from these savings if FedNow is adopted widely. Using innovation productively and responsibly in this way could make banking services more inclusive.

However, the White House acknowledges that FedNow does indeed open the door for a possible CBDC, also citing Fed Governor Bowman (see above quote).

As for a CBDC, the White House also has good things to say about implementing one:

A U.S. CBDC—a digital form of the U.S. dollar—would have the potential to offer significant benefits. It could enable a payment system that is more efficient, provide a foundation for further technological innovation, facilitate faster cross-border transactions, and be environmentally sustainable.

It could also promote financial inclusion and equity by enabling access for a broad range of consumers. A potential U.S. CBDC could also help support other policy goals. For example, a potential U.S. CBDC could help ensure that such payment systems are aligned with the principles of human rights, democratic values, and privacy.

They do, however, also notate that the introduction of a CBDC would mean that certain “permissions” would be attached to them. In other words, a social credit score perhaps, or term limits and clauses that provide a framework as to how the CBDCs can be spent, used, and saved. CBDCs have expiration dates, for example, so the idea of saving and being frugal with them are canned.

The document explains:

A White House assessment of a potential U.S. CBDC system recently noted that “while a U.S. CBDC system could, in theory, be mostly ‘permissionless’ from a governance standpoint, this design choice introduces a large number of technical complexities and practical limitations that strongly suggest a permissionless approach does not make sense for a system that has at least one trusted entity (i.e., the central bank).”

This is somewhat ironic, given that this is different from an oft-cited founding principle of crypto assets like Bitcoin, whose purported aim was to create decentralized money without any trusted central authority.

In conclusion, while these systems are worked on and fine tuned, “In the meantime, some crypto assets appear to be here to stay, and they continue to cause risks for financial markets, investors, and consumers,” the White House says.

In the end, the Biden administration claims that there is value in both FedNow and/or a CBDC:

Certain innovations, such as FedNow and a potential U.S. CBDC, could help bring the U.S. financial infrastructure into the digital era in a clear and simple way, without the risks or irrational exuberance brought by crypto assets. Hence, continued investments in the Nation’s financial infrastructure have the potential to offer significant benefits to consumers and businesses, but regulators must apply the lessons that civilization has learned, and thus rely on economic principles, in regulating crypto assets

The White House wrote

While the Federal Reserve claims that FedNow has nothing to do with a CBDC, it is no secret that they are working on one.

The Federal Reserve has already engaged in the creation of their own CBDC with major U.S. banks and credit card companies, reported by The WP last year.

Moreover, months prior to that, the Fed announced that they would be working on a carbon-based social credit score investing platform with some of the largest banks in the country.

SEE: BRICS Nations Discussing Working On A ‘Fundamentally New Currency’ According To Russian Official

AUTHOR COMMENTARY

The rich man is wise in his own conceit; but the poor that hath understanding searcheth him out.

Proverbs 28:11

Clearly the Federal Reserve is lying, especially when you have the White House admitting that the two are related. The system is so obviously designed to facilitate a CBDC. Don’t ever take the Fed or rich bankster gangsters serious: they never tell the whole truth; though the government does not either, but you get my point.

The White House, if you read the rest of the section on cryptos, are basically admitting that the proliferation of these decentralized currencies were designed to grease the wheels of the masses, to get them used to the idea of a digital currency – one that the central bank would eventually oversee and regulate.

The introduction of a CBDC is inevitable, but it will not happen overnight: it will progressively be fostered in after FedNow is launched, and once the financial markets and the everything bubble is allowed to pop, and the people are begging for bread, then the talks of a CBDC will become loud. And the people will accept it, sad to say.

Ways To Resist And Slowdown The Introduction Of Central Bank Digital Currencies

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

Hi! Do you know if they make any plugins to assist with SEO? I’m trying to get my blog to rank for some targeted keywords but I’m not seeing very good gains. If you know of any please share. Cheers!

Hello, Neat post. There’s a problem along with your web site in web explorer, could test thisK IE nonetheless is the marketplace leader and a huge component to other people will miss your fantastic writing because of this problem.

Wonderful site. Lots of helpful information here. I am sending it to several buddies ans also sharing in delicious. And certainly, thank you to your sweat!

Magnificent website. Plenty of helpful info here. I am sending it to several friends ans additionally sharing in delicious. And of course, thank you on your effort!

Wonderful beat ! I wish to apprentice at the same time as you amend your web site, how can i subscribe for a weblog web site? The account aided me a applicable deal. I have been tiny bit familiar of this your broadcast provided vibrant transparent idea

Very interesting details you have observed, thanks for putting up.

Hi there! I’m at work browsing your blog from my new iphone 3gs! Just wanted to say I love reading your blog and look forward to all your posts! Keep up the outstanding work!

hi!,I love your writing very a lot! share we keep up a correspondence extra approximately your article on AOL? I require a specialist in this space to unravel my problem. Maybe that is you! Having a look ahead to peer you.

Hmm is anyone else having problems with the images on this blog loading? I’m trying to figure out if its a problem on my end or if it’s the blog. Any responses would be greatly appreciated.

Hi there! Someone in my Myspace group shared this website with us so I came to give it a look. I’m definitely loving the information. I’m bookmarking and will be tweeting this to my followers! Terrific blog and superb design and style.

I just like the helpful information you provide on your articles. I will bookmark your blog and take a look at again right here regularly. I am moderately certain I will be told many new stuff right here! Good luck for the next!

F*ckin’ remarkable things here. I’m very glad to see your article. Thanks a lot and i am looking forward to contact you. Will you please drop me a e-mail?

My brother suggested I might like this blog. He was entirely right. This post truly made my day. You cann’t imagine simply how much time I had spent for this information! Thanks!

You made some good points there. I looked on the internet for the subject and found most people will approve with your site.

Hi, I think your blog might be having browser compatibility issues. When I look at your blog in Ie, it looks fine but when opening in Internet Explorer, it has some overlapping. I just wanted to give you a quick heads up! Other then that, excellent blog!

Wow, wonderful weblog format! How long have you been blogging for? you made running a blog glance easy. The entire glance of your site is magnificent, as well as the content material!

When I initially commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get three e-mails with the same comment. Is there any way you can remove me from that service? Thanks!

Wow! This could be one particular of the most useful blogs We have ever arrive across on this subject. Basically Wonderful. I am also a specialist in this topic therefore I can understand your effort.

Great post. I am facing a couple of these problems.

You actually make it appear really easy together with your presentation but I in finding this matter to be actually one thing that I feel I’d never understand. It seems too complex and extremely vast for me. I am looking ahead on your subsequent publish, I¦ll attempt to get the grasp of it!

Have you ever thought about adding a little bit more than just your articles? I mean, what you say is important and everything. But think about if you added some great pictures or videos to give your posts more, “pop”! Your content is excellent but with images and video clips, this website could certainly be one of the best in its field. Excellent blog!

magnificent points altogether, you simply received a logo new reader. What could you suggest in regards to your put up that you made a few days in the past? Any sure?

My coder is trying to convince me to move to .net from PHP. I have always disliked the idea because of the expenses. But he’s tryiong none the less. I’ve been using Movable-type on a variety of websites for about a year and am concerned about switching to another platform. I have heard great things about blogengine.net. Is there a way I can transfer all my wordpress posts into it? Any kind of help would be really appreciated!

I like this web site because so much useful material on here : D.

Some truly nice and useful information on this web site, also I think the style and design has got great features.

Once I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get 4 emails with the identical comment. Is there any manner you may remove me from that service? Thanks!

There is noticeably a bundle to know about this. I assume you made certain nice points in features also.

Pretty component to content. I just stumbled upon your website and in accession capital to assert that I get in fact loved account your weblog posts. Anyway I will be subscribing in your augment or even I fulfillment you access persistently rapidly.

It’s a pity you don’t have a donate button! I’d certainly donate to this fantastic blog! I suppose for now i’ll settle for bookmarking and adding your RSS feed to my Google account. I look forward to brand new updates and will share this website with my Facebook group. Chat soon!

I got what you mean ,bookmarked, very decent website .

What i don’t understood is in truth how you are no longer actually a lot more well-preferred than you might be now. You are so intelligent. You recognize therefore significantly with regards to this matter, produced me individually believe it from so many varied angles. Its like women and men aren’t interested except it is something to do with Lady gaga! Your individual stuffs great. At all times deal with it up!

You really make it appear really easy together with your presentation but I find this matter to be really something that I believe I might by no means understand. It sort of feels too complex and very broad for me. I am taking a look forward for your next publish, I will attempt to get the hang of it!

When I originally commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove people from that service? Thanks a lot!

Perfect piece of work you have done, this internet site is really cool with great information.

Some really nice and utilitarian info on this website , likewise I think the pattern holds fantastic features.

you’re really a good webmaster. The site loading speed is incredible. It seems that you’re doing any unique trick. Moreover, The contents are masterwork. you have done a great job on this topic!

Hello my family member! I want to say that this article is amazing, great written and come with almost all important infos. I’d like to look extra posts like this.