In April of this year, I explained how the data does not support a housing crash in the United States. As much as people want prices to fall precipitously, especially Millennials and Zoomers, the numbers simply disprove a housing crash; as prices continue to go up and home affordability worsens as homelessness rises, while institutional buying continues to happen unabated and illegals are being gifted easy money and zero credit to buy a home.

Admittedly, a lot of what I said in April will be on repeat here again but with more up-to-date numbers. This is important to highlight because there are still a lot of social media influencers and self-proclaimed financial gurus who are simply peddling misinformation and clickbait, or trying to sell their audience useless courses to capitalize on an imminent housing crash. I’m not going to get overly technical, not that I need to be. I also am not a “financial guru,” but I’d like to think that I am not a fool either.

To keep things short and sweet, it comes down to the basics: supply and demand. Right now we have volcano-hot demand, and supply that simply cannot keep up for a number of reasons: unattainable prices and mortgage rates, institutional buying for pennies on the dollar, or even things such as older generations less willing to downsize their homes and close on a deal for a price less than the estimated value.

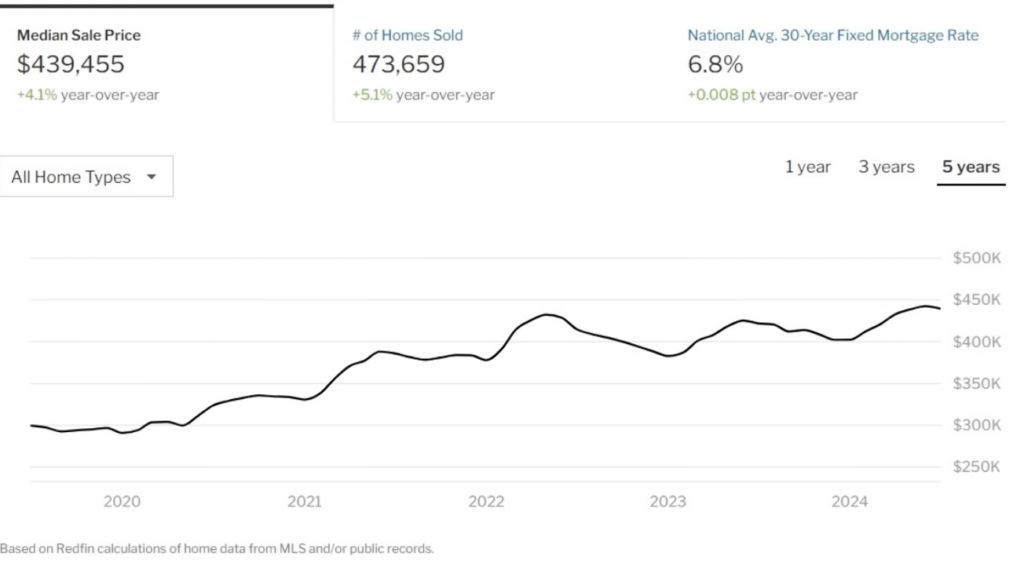

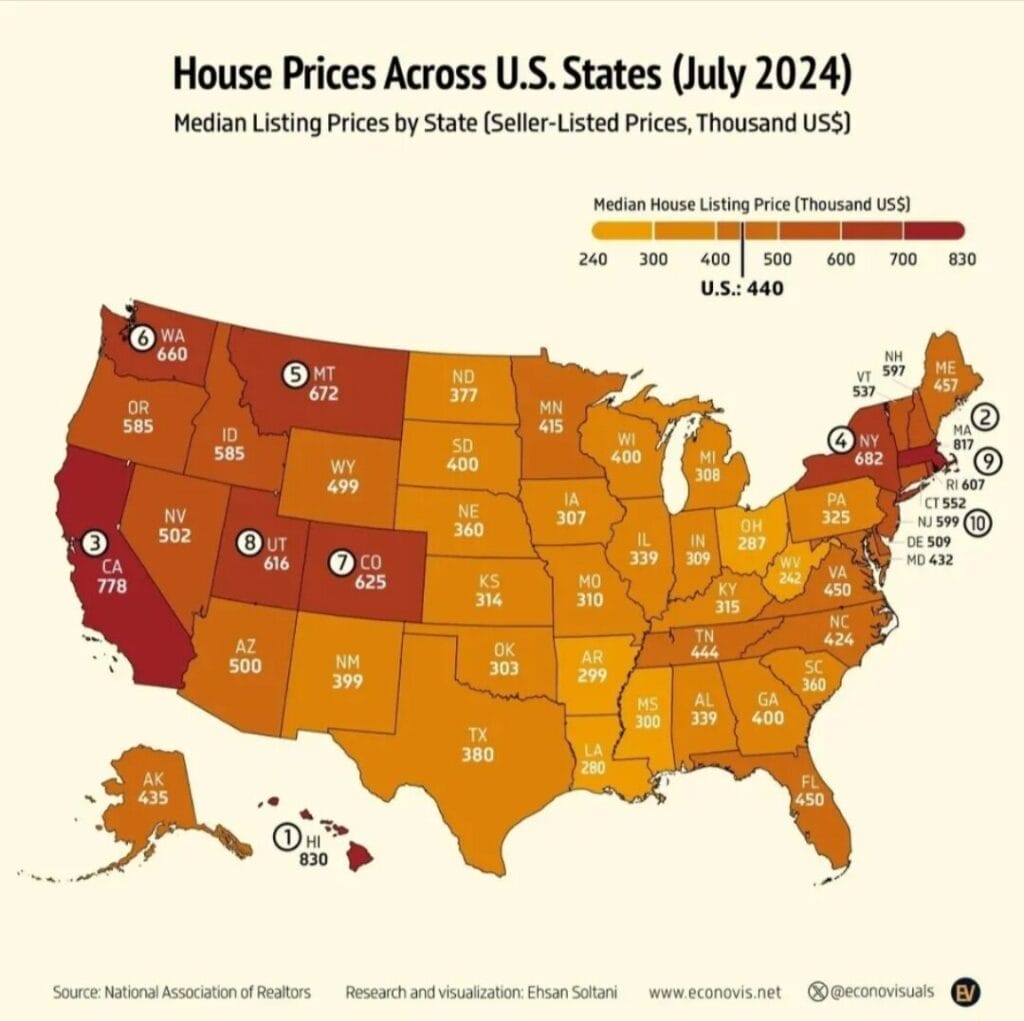

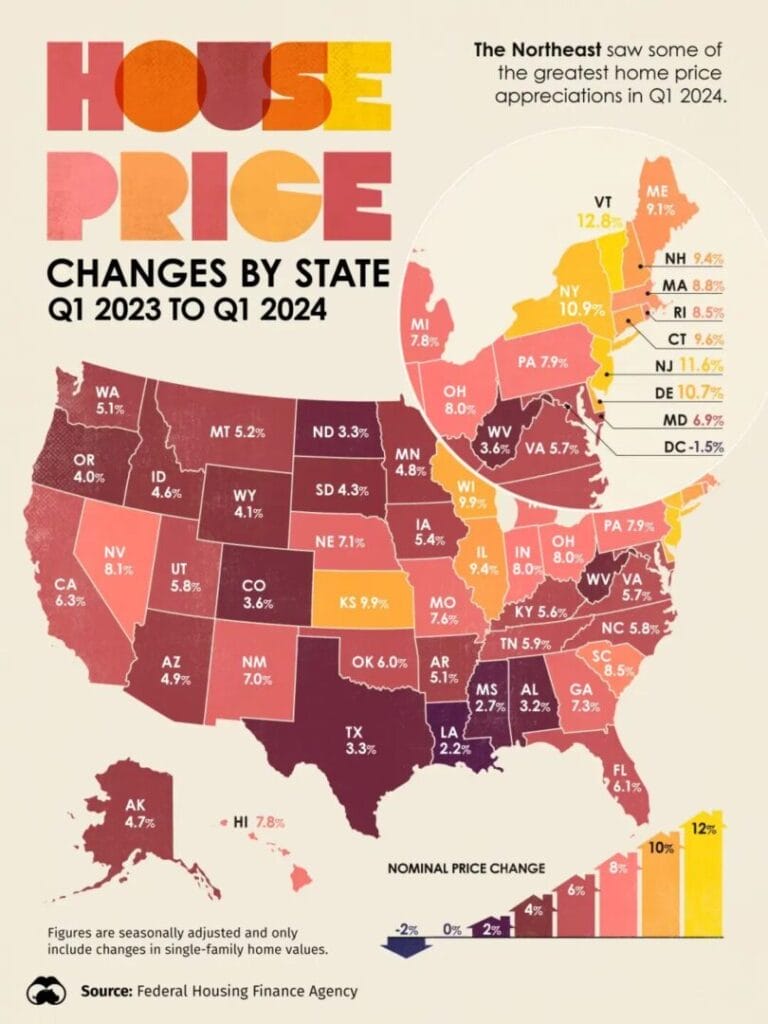

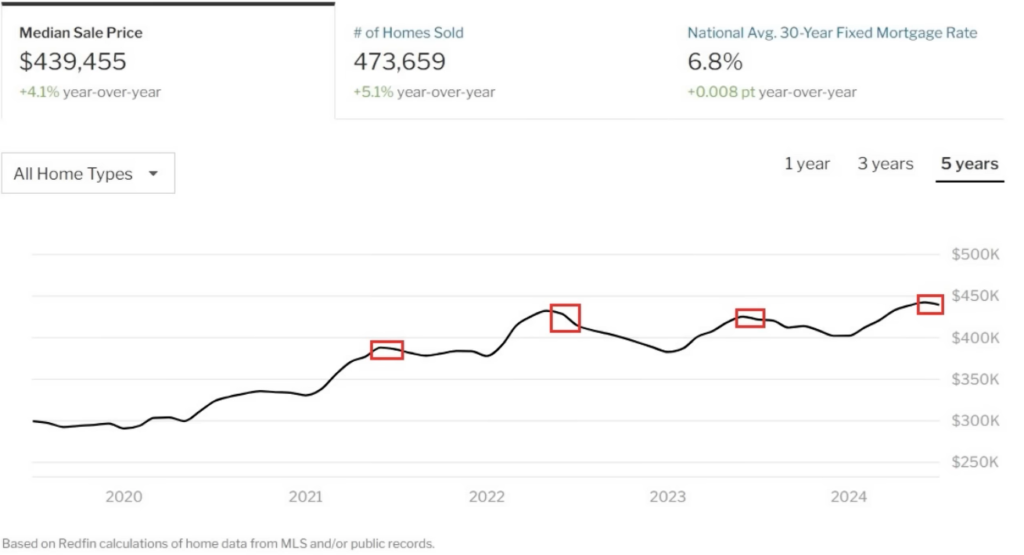

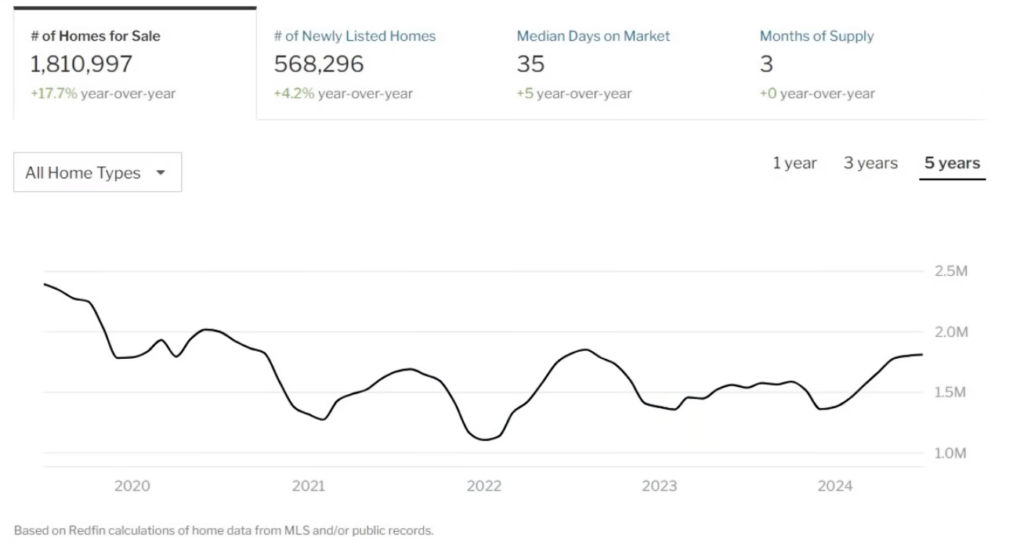

According to Redfin, the median average price in the U.S. sits at $439,455 dollars. This is an increase from the $412K price tag I reported in April. In the span of five years home prices have increased 47%. Here are some charts that highlight the price of homes by state and by how much they have increased.

The “rub” comes when a lot of these clickbaiters and crash callers highlight how in certain areas and counties prices are dropping quickly. And while that may be true for specific regions, and that’s great and all, the data plainly shows that prices continue to trend upward nationally, just as inflation continues to still tick up steadily and remain high (grossly higher than the government would ever care to admit).

Like last time, Brian Kim, CPA, from ClearValue Tax refutes some of the common arguments that could be used to peddle the notion that a housing crash is imminent.

As Brian highlights, the slight dip seen on the chart courtesy of Redfin is congruent with prices around this time over the last several years, demonstrating a seasonal trend.

For those that may argue that a rise in foreclosures will trigger a housing crash, just as it did in 2008, foreclosures in 2024 and this decade so far are significantly down from the rapid rate of foreclosures experienced during the Great Recession and subsequent fallout. ATTOM reported in 2008, 1,332,991 foreclosures were recorded, with millions more to follow. But foreclosures are currently at 177,431 so far this year. Therefore, a crash will not occur due to foreclosures.

The data, according to Redfin, also shows that there is less supply compared to two years ago, and even less than that when compared to 2020. As I said earlier, demand is very high but supply is limited. So a crash cannot happen this way either.

Brian explained that perhaps a crash could occur should supply greatly increase due to a “nasty recession,” where millions more Americans become unemployed and the economy completely tanks. But Brian says this is “sincerely close to impossible.”

Jerome Powell and the Federal Reserve recently declared that they are basically (without saying it) trashing their 2% inflation mandate they kept talking about for a while, and will begin to pivot in September and start cutting rates and more going into next year, and will print more helicopter money on top of it (quantitative easing). Powell declared that “the time has come” to make the pivot.

The time has come for policy to adjust. We do not seek or welcome further cooling in the labor market. We will do everything we can to support a strong labor market as we make further progress toward price stability.

Powell said at a meeting in Jackson Hole, Wyoming last week

The announcement came off the back of the revised jobs report numbers that erased 818,000 jobs off the board, forcing us to once again call poppycock on the numbers we have been getting. After all, Powell and the Feds regularly say they are “data dependent.” Additionally, we know that inflation is significantly higher than what is being reported.

Meanwhile, mortgage rates in the U.S. are already going down, with a 15-year sitting at slightly above 5.6% and 6.46% for a 30-year mortgage, according to Freddie Mac.

Simply put, in this current environment and moving forward, home prices will only continue to rise. Lowering rates and printing more Monopoly money is inflationary, and therefore would be counterintuitive for a housing crash.

Again, give Brian’s video a watch.

For conditions to improve to get affordable housing things need to get fixed, but they are not getting fixed. We need to build more homes, we need to reduce inflation, wage growth needs to grow faster than the cost of living, and the labor market needs to improve.

But the housing shortage persists, inflation is ongoing, real wage growth is not keeping up with the pace of inflation, and the labor market is deteriorating. Would you prefer that I lie to you like politicians?

Brian said in his video

Also, as I reported last time in April, Brian pointed out that “if home prices are down 26% in your area, that means that homes prices are up by 26% in a different area. If you don’t believe in math, then what I can say? I’m not going to argue with you.” He’s not wrong; and the same wisdom applies to something like the stock market: in order to earn money someone hast to lose money. This is a truism that is vaguely understood and seldomly explained.

But Brian is certainly not the only one saying this. From my report in April:

As explained plainly by Bankrate in March: ‘No. There are still far more buyers than sellers, and that means a meaningful price decline can’t happen: “There’s just generally not enough supply,” says Mark Fleming, chief economist at title insurer First American Financial Corporation. “There are more people than housing inventory. It’s Econ 101.”’

Dave Liniger, the founder of real estate brokerage RE/MAX, said: “You’ve got an entire generation of pent-up demand. We’re in this fascinating position of tremendous demand and too little inventory. When interest rates do start to come down, it’ll be another boom-and-bust cycle.”

Prices will remain firm and will not decline on a national level.

Lawrence Yun, Chief Economist, National Association of Realtors

This is what The Trends Journal forecasted in December, 2023, writing:

When the U.S. Federal Reserve begins cutting interest rates in the first part of next year, more homes will come onto the market as homeowners now sitting on low-rate mortgages will find themselves able to afford mortgages on new digs. That will put more homes on the market but also boost the number of potential buyers for them.

Therefore, prices nationally will stay high and possibly keep rising. People with the most cash and best credit will secure funding and shut out people who, in a normal housing market, would be able to own a home of their own.

And even before that forecast, The TJ had been saying for a couple of years before this one that there would not be a crash, accurately saying “housing prices would fall but not crash. The shortage of homes for sale has kept buyers bidding against each other for the few available.” Of course now, before interest rates have even been cut, housing prices are still ticking upwards.

Lower interest rates will bring more of those frustrated would-be buyers into the market. However, home prices will remain elevated even then: demand will still outpace supply and many sellers will be unwilling to accept a price significantly lower than today’s boom time.[…] Because home prices and mortgage interest rates are high, and will remain so at least through this year, first-time and modest-income buyers will continue to be denied their chance at the American Dream of home ownership and the opportunity to build wealth in the way that most Americans have in the past.

The magazine added

Moreover, in April, Creditnews published a detailed report on housing affordability across the country, and while there are some ‘deals’ (in relative terms) to be had, they say “what we discovered reveals the story of two Americas: one where middle-class families can still qualify for an average home and one where they’ve been priced out entirely.”

There’s no two ways about it: Housing affordability has worsened significantly since Covid. In 2019, middle-class households could comfortably buy a typical home in 91 of the top 100 largest metros. By 2024, that figure had fallen to just 52. Families in the lower middle class can only afford to buy an average home in 7 of the top 100 metros.Sam Bourgi, Senior Analyst at Creditnews

In short, as Bankrate points out, there are five main reasons why a housing crash will not occur:

- Inventories are still very low

- Builders didn’t build quickly enough to meet demand

- Demographic trends are creating new buyers

- Lending standards remain strict

- Foreclosure activity is muted

Should a housing crash even occur, and even if it’s a really deep one, prices will still be well out of target range and affordability for a mortgage.

Per the recent data, these factors have remained true.

As I said earlier, you also have to factor in that institutional buying is at fever pitch, thanks to the likes of Blackrock, Blackstone, Vanguard, and State Street. These groups, among others, are buying entire swaths of homes and neighborhoods, particularly single-family starter homes and renting them out, further driving up rental costs.

SEE: Bought & Paid For: Joe Biden Is Bankrolled By Blackrock And Donald Trump Is Bankrolled By Blackstone

As Brian said earlier this year: “We are moving towards a nation of renters. It’s not going to be overnight, but slow and steady wins the race for big institutions.”

Lena Petrova, CPA, has said something similar in her reports on the housing market; while homelessness continues to rise, immigrants and illegals continue to flood the country invited, while the standard of living continues to erode. These problems are being felt across the Western world, with rent costs soaring as well.

Check out her videos below (though some of the numbers are slightly out of date already):

Clearly, the so-called “American Dream” is dead; and in the words of George Carlin, “you have to be asleep to believe it.” I recently reported on an article the Wall Street Journal did that lauded the World Economic Forum’s dystopian message: “You’ll own nothing and be happy.”

SEE: Wall Street Journal Lauds America’s ‘Extreme Renters Who Own Nothing,’ Including Their Own Clothes

And yet we continue to hear from clickbaiters and sensationalists who still persist in lying and exaggerating the data to promote an imminent housing market crash.

In April, Brian went after some of these crash callers, blasting them and making fools of them. In particular, he went after Graham Stephan, a popular financial channel on YouTube, who has been repeatedly calling for an imminent housing crash that has never come to pass, even just recently saying there’d be one this year.

Stephan was the only one Brian namedropped, calling him a “feminine little boy with a Napoleon complex,” because apparently Stephan dogged on Brian a while ago.

But his main reason for doing this response is because of the people who come to Brian’s channel confused because they got misled by these clickbait videos pumping hopium and misinformation.

And lo and behold, Graham is still promoting a housing market crash per a video he posted in July, saying the crash will be in 2026.

This time around, however, people have become more privy to these tall tales.

I’ll add to this list some of the people I’ve seen peddling the imminent crash calling:

In February, I called out and exposed “The Economic Ninja” (Travis Barjema) for this very thing, selling courses with grifter-like and fraudulent tactics, getting all emotional and using Bible verses to try to sound genuine and sincere.

Another one is Kevin Paffrath, better known as “Meet Kevin.”

Another one is “Reventure Consulting” (Nick Gerli).

There are many more but these are just a small sampling. And then on the flipside you’ve got “boomer meme” Dave Ramsey and crew, who keep telling people to buy a home every waking second it feels like.

Romans 16:17 Now I beseech you, brethren, mark them which cause divisions and offences contrary to the doctrine which ye have learned; and avoid them. [18] For they that are such serve not our Lord Jesus Christ, but their own belly; and by good words and fair speeches deceive the hearts of the simple.

That’s how the conmen do it. They go after the innocent and ignorant, all for clicks, clout, and quick cash. It’s dog-eat-dog: they need suckers to go broke or be distracted as to level the playing field. Again, in order to win money in markets one must lose money.

Proverbs 20:14 It is naught, it is naught, saith the buyer: but when he is gone his way, then he boasteth. [15] There is gold, and a multitude of rubies: but the lips of knowledge are a precious jewel.

As I said with Ninja – Verse is 14 is the credo of all get-rich-quick, Ponzis, and other greedy scams, and it absolutely fits like a glove here with Ninja. By the way the verse is written the inverse is true. The seller comes along and says, “my [such and such] will change your life. You need it; but if you want to stay broke, then don’t buy it: but if you want to be rich like me, then buy now before it’s too late!” The same applies to this housing market hopium.

Again, supply and demand. Demand must crater significantly; and the only potential way this happens is there would be a mass-culling of the population, though even that still does not discount the institutional buyers who can buy up the Monopoly board unconstrained.

Having said that – to the saved, be aware and be vigilant, but don’t fret yourself and wait on the Lord. Patience is key here, as with everything; and I hope to, Lord willing, further discuss these topics in future studies with the scriptures as to what’s going to happen with the economies of the world, and what we can do about it…

Psalm 37:7 Rest in the LORD, and wait patiently for him: fret not thyself because of him who prospereth in his way, because of the man who bringeth wicked devices to pass. [8] Cease from anger, and forsake wrath: fret not thyself in any wise to do evil.

Proverbs 24:19 Fret not thyself because of evil men, neither be thou envious at the wicked; [20] For there shall be no reward to the evil man; the candle of the wicked shall be put out.

Proverbs 29:16 When the wicked are multiplied, transgression increaseth: but the righteous shall see their fall.

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

Thank you for warning. I forwarded your article on gold scams to Dr. Jane Ruby who also put Agusta Precious Metal stuff on her channel kn rumble.com. I never got a reply. I guess I was fooled by PhD not medicine doctor.

You are welcome. I would like to think that some of these people might just be completely ignorant and do not know how this stuff works, but a lot of them are just greedy and are only counting the zeros at the end of the check.

10 to 20 million mostly subsidized illegals in the country. They eat on our dime and drive up grocery prices and they all need a roof over their head. Most people are blind to this simple economic disruption.

Мне понравилась организация статьи, которая позволяет легко следовать за рассуждениями автора.

Автор старается оставаться нейтральным, предоставляя информацию, не оказывающую явного влияния на читателей.

Автор статьи представляет сведения, опираясь на факты и экспертные мнения.

I know this if off topic but I’m looking into starting my own blog and was curious what all is required to get set up? I’m assuming having a blog like yours would cost a pretty penny? I’m not very web savvy so I’m not 100 sure. Any recommendations or advice would be greatly appreciated. Appreciate it

Мне понравился объективный и непредвзятый подход автора к теме.

Hey I know this is off topic but I was wondering if you knew of any widgets I could add to my blog that automatically tweet my newest twitter updates. I’ve been looking for a plug-in like this for quite some time and was hoping maybe you would have some experience with something like this. Please let me know if you run into anything. I truly enjoy reading your blog and I look forward to your new updates.

Статья предлагает конкретные примеры, чтобы проиллюстрировать свои аргументы.

Я хотел бы отметить глубину исследования, представленную в этой статье. Автор не только предоставил факты, но и провел анализ их влияния и последствий. Это действительно ценный и информативный материал!

Admiring the time and effort you put into your blog and detailed information you offer. It’s awesome to come across a blog every once in a while that isn’t the same unwanted rehashed material. Excellent read! I’ve bookmarked your site and I’m including your RSS feeds to my Google account.

Эта статья является настоящим источником вдохновения и мотивации. Она не только предоставляет информацию, но и стимулирует к дальнейшему изучению темы. Большое спасибо автору за его старания в создании такого мотивирующего контента!

Это способствует более глубокому пониманию и анализу представленных фактов.

It’s awesome to visit this web page and reading the views of all colleagues on the topic of this post, while I am also keen of getting familiarity.

Автор предлагает практические советы, которые читатели могут использовать в своей повседневной жизни.

Автор старается быть балансированным, предоставляя достаточно контекста и фактов для полного понимания читателями.

Everything is very open with a precise description of the challenges. It was truly informative. Your site is very useful. Many thanks for sharing!

Статья помогла мне лучше понять сложные взаимосвязи в данной теме.

Автор представляет информацию в легком и доступном формате, что делает ее приятной для чтения.

Я только что прочитал эту статью, и мне действительно понравилось, как она написана. Автор использовал простой и понятный язык, несмотря на тему, и представил информацию с большой ясностью. Очень вдохновляюще!

Мне понравилась глубина исследования, представленная в статье.

Автор старается сохранить нейтральность и оставляет решение оценки информации читателям.

I do accept as true with all the concepts you have presented to your post. They are very convincing and can definitely work. Nonetheless, the posts are too quick for novices. Could you please extend them a little from next time? Thank you for the post.

Автор статьи предоставляет важные сведения и контекст, что помогает читателям более глубоко понять обсуждаемую тему.

Это позволяет читателям анализировать представленные факты самостоятельно и сформировать свое собственное мнение.

Очень хорошо исследованная статья! Она содержит много подробностей и является надежным источником информации. Я оцениваю автора за его тщательную работу и приветствую его старания в предоставлении читателям качественного контента.

Статья предлагает широкий обзор темы, представляя разные точки зрения и подробности.

Мне понравился баланс между фактами и мнениями в статье.

Я оцениваю информативность статьи и ее способность подать сложную тему в понятной форме.

Я оцениваю тщательность и точность, с которыми автор подошел к составлению этой статьи. Он привел надежные источники и представил информацию без преувеличений. Благодаря этому, я могу доверять ей как надежному источнику знаний.

Мне понравился нейтральный тон статьи, который позволяет читателю самостоятельно сформировать мнение.

Это позволяет читателям получить разностороннюю информацию и самостоятельно сделать выводы.

Мне понравился объективный подход автора, который не пытается убедить читателя в своей точке зрения.

Автор представляет свои идеи объективно и не прибегает к эмоциональным уловкам.

Автор предлагает подробное объяснение сложных понятий, связанных с темой.

Я оцениваю объективность и непредвзятость автора в представлении информации.

Читателям предоставляется возможность ознакомиться с различными точками зрения и принять информированное решение.

Я прочитал эту статью с огромным интересом! Автор умело объединил факты, статистику и персональные истории, что делает ее настоящей находкой. Я получил много новых знаний и вдохновения. Браво!

Мне понравилось, как автор представил информацию в этой статье. Я чувствую, что стал более осведомленным о данной теме благодаря четкому изложению и интересным примерам. Безусловно рекомендую ее для прочтения!

Hmm is anyone else experiencing problems with the images on this blog loading? I’m trying to figure out if its a problem on my end or if it’s the blog. Any suggestions would be greatly appreciated.

Статья предлагает широкий обзор темы, представляя разные точки зрения и подробности.

Автор статьи предоставляет подробное описание событий и дополняет его различными источниками.