The following report is by KFF Health News, via CBS News:

The Biden administration announced a major initiative to protect Americans from medical debt on Thursday, outlining plans to develop federal rules barring unpaid medical bills from affecting patients’ credit scores.

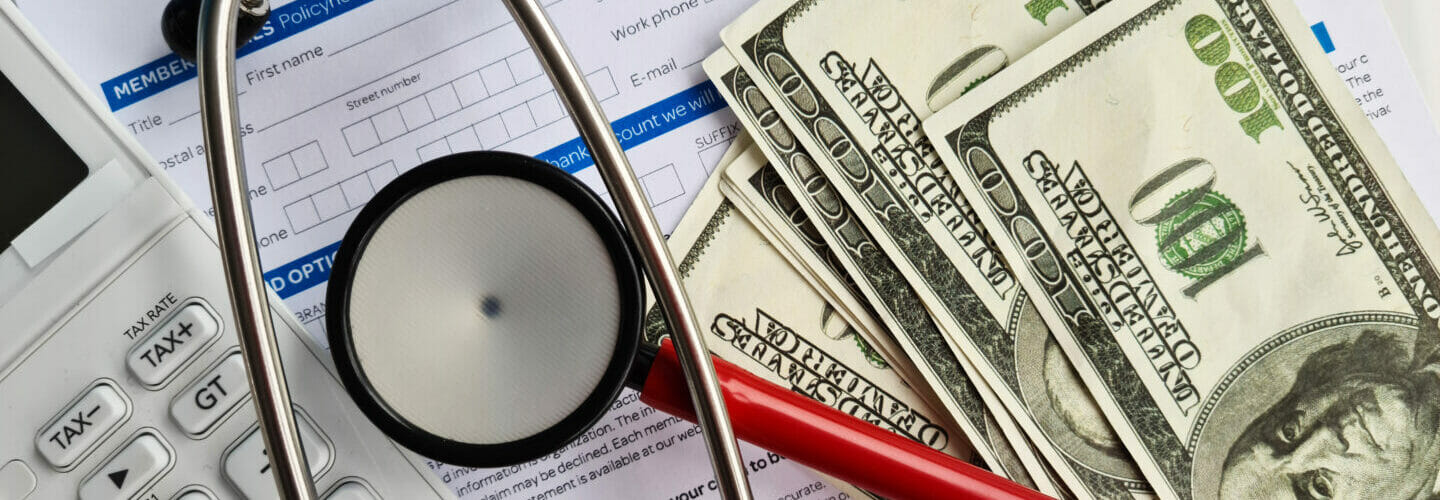

The regulations, if enacted, would potentially help tens of millions of people who have medical debt on their credit reports, eliminating information that can depress consumers’ scores and make it harder for many to get a job, rent an apartment, or secure a car loan.

New rules would also represent one of the most significant federal actions to tackle medical debt, a problem that burdens about 100 million people and forces legions to take on extra work, give up their homes, and ration food and other essentials, a KFF Health News-NPR investigation found.

No one in this country should have to go into debt to get the quality health care they need.

These measures will improve the credit scores of millions of Americans so that they will better be able to invest in their future.

Vice President Kamala Harris, said, who announced the new moves along with Rohit Chopra, head of the Consumer Financial Protection Bureau, or CFPB. The agency will be charged with developing the new rules.

Enacting new regulations can be a lengthy process. Administration officials said Thursday that the new rules would be developed next year.

Such an aggressive step to restrict credit reporting and debt collection by hospitals and other medical providers will also almost certainly stir industry opposition.

At the same time, the Consumer Financial Protection Bureau, which was formed in response to the 2008 financial crisis, is under fire from Republicans, and its future may be jeopardized by a case before the Supreme Court, whose conservative majority has been chipping away at federal regulatory powers.

But the move by the Biden administration drew strong praise from patients’ and consumer groups, many of whom have been pushing for years for the federal government to strengthen protections against medical debt.

This is an important milestone in our collective efforts and will provide immediate relief to people that have unfairly had their credit impacted simply because they got sick.

Emily Stewart, executive director of Community Catalyst, a Boston nonprofit that has helped lead national medical debt efforts, said

Credit reporting, a threat designed to induce patients to pay their bills, is the most common collection tactic used by hospitals, a KFF Health News analysis has shown.

Negative credit reporting is one of the biggest pain points for patients with medical debt. When we hear from consumers about medical debt, they often talk about the devastating consequences that bad credit from medical debts has had on their financial lives.

Said Chi Chi Wu, a senior attorney at the National Consumer Law Center.

Although a single black mark on a credit score may not have a huge effect for some people, the impact can be devastating for those with large unpaid medical bills. There is growing evidence, for example, that credit scores depressed by medical debt can threaten people’s access to housing and fuel homelessness in many communities.

At the same time, CFPB researchers have found that medical debt — unlike other kinds of debt — does not accurately predict a consumer’s creditworthiness, calling into question how useful it is on a credit report.

The three largest credit agencies — Equifax, Experian, and TransUnion — said they would stop including some medical debt on credit reports as of last year. The excluded debts included paid-off bills and those less than $500.

But the agencies’ voluntary actions left out millions of patients with bigger medical bills on their credit reports. And many consumer and patient advocates called for more action.

The National Consumer Law Center, Community Catalyst, and some 50 other groups in March sent letters to the CFPB and IRS urging stronger federal action to rein in hospital debt collection.

State leaders also have taken steps to expand consumer protections. In June, Colorado enacted a trailblazing bill that prohibits medical debt from being included on residents’ credit reports or factored into their credit scores.

Many groups have urged the federal government to bar tax-exempt hospitals from selling patient debt or denying medical care to people with past-due bills, practices that remain widespread across the U.S., KFF Health News found.

Hospital leaders and representatives of the debt collection industry have warned that such restrictions on the ability of medical providers to get their bills paid may have unintended consequences, such as prompting more hospitals and physicians to require upfront payment before delivering care.

Looser credit requirements could also make it easier for consumers who can’t handle more debt to get loans they might not be able to pay off, others have warned.

It is unfortunate that the CFPB and the White House are not considering the host of consequences that will result if medical providers are singled out in their billing, compared to other professions or industries.

Scott Purcell, chief executive of ACA International, the collection industry’s leading trade association, said

AUTHOR COMMENTARY

[26] Be not thou one of them that strike hands, or of them that are sureties for debts. [27] If thou hast nothing to pay, why should he take away thy bed from under thee? Proverbs 22:26-27

This absurdity, if allowed to go through, is another drop of the anvil on Americans, most of whom will think this is a great idea, even if they hate Biden’s guts.

Again, similarly to how Biden wanted to cancel student debt (which failed), it would have meant Americans who were not in debt would have had to flip the bill for that. Even though that ultimately failed, it was used as a mechanism to buy votes on hope based on lies; and this latest action if allowed to proceed is designed to buy votes of ignorant people who think this is grand.

If these debts are removed from people’s credit scores then you will see banks even more unlikely to lend and loan cash (at a time when banks are tightening lending as is), because they can no longer trust the customer’s credit scores. Therefore borrowing costs and other fees will increase for everyone else.

This will cause even more economic woes, heading into a time where we will be dealing with a full-blow depression.

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

Med debt doesn’t effect your score if ya pay regularly, if ya have it just send them what ya can. Med debt has never messed with my score. There isn’t anyone that can absorb med debt, that is middle or poor class even with insurance. Be careful with med, they have so many ways to screw ya over.

Trust me on this, just send them what ya can and they will leave ya credit alone.

But this has been my experience only; take it with a grain of salt.