The volatility within the thousands of U.S. banks, small, medium, and large is indeed fascinating.

In mid-May, according to public data published by the St. Louis Federal Reserve, an astounding $910 billion in deposits fled American financial institutions, compared to one year ago at that time. Financial and crypto website Daily Hodl reported at the time, ‘In May of last year, the amount of capital held by banks on behalf of depositors sat at $18.06 trillion. Today, that number is down to $17.15 trillion. And in the last week, $13 billion has exited the system,’ the outlet noted.

This trend was reconfirmed by the Federal Deposit Insurance Corporation (FDIC) in early June, revealing the numbers for Quarter 1 of economic activity; reporting depositors withdrew $472 billion from their banks accounts in the first quarter of this year – breaking a 39-year record.

The quarterly decline is the largest reduction reported in the QBP since data collection began in 1984.

This was the fourth consecutive quarter that the industry reported lower levels of total deposits.

The FDIC wrote in their statement

But then the volatility really became pronounced and thus began this wild roller coaster ride:

Nearly two weeks later that trend completely reversed and $133.16 billion was reportedly injected into the banking sector, according to data from the Federal Reserve. By mid-June it was revealed that outflows starkly rose once again as $79.16 billion exited American bank accounts.

The hilly ride continued in early July with almost $47 billion entering the U.S. banking system. Then by mid-July the Feds disclosed that $78,000,000,000 fled the system.

By early August, on the heels of the collapse of Heartland Bank and PacWest, it was revealed that megabanks JPMorgan Chase, Bank of America, Citigroup and Wells Fargo saw $262 billion in deposit flights versus the same period in 2022, according to Yahoo Finance.

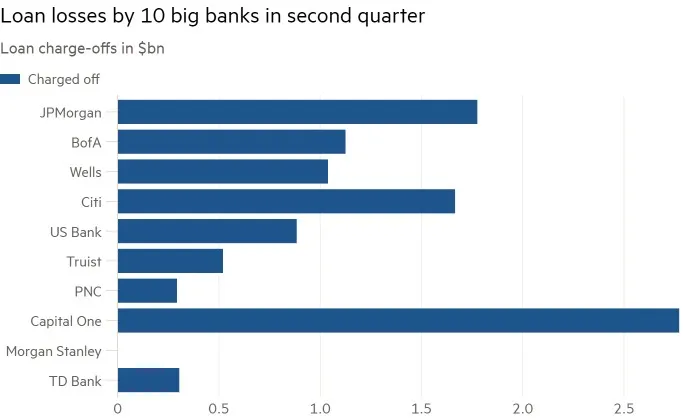

More recently, the Financial Times reported that JPMorgan Chase, Capital One and others lost a combined $18.9 billion in Q2 of 2023 due to bad loans.

This announcement also came on the heels that financial ratings manager Moody’s downgraded 10 more banks that are speculated to have notable liquidity problems and bad credit. With that announcement Moody’s warned that deposit flights are most likely to continue as interest rates remain elevated and expected to rise again. The firm stated:

US banks continue to contend with interest rate and asset-liability management (ALM) risks with implications for liquidity and capital, as the wind-down of unconventional monetary policy drains systemwide deposits and higher interest rates depress the value of fixed-rate assets…

Although the general drain on deposit funding caused by quantitative tightening (QT) moderated in Q2, there remains a significant risk that systemwide deposits will resume their decline in coming quarters. Most banks’ deposits were flat or down only modestly, but the mix worsened, with non-interest-bearing deposits declining and banks paying more for deposits. The resulting drop in net interest income and net interest margins eroded profitability and, thus, the ability to replenish capital internally.

Meanwhile, many banks’ Q2 results showed growing profitability pressures that will reduce their ability to generate internal capital. This comes as a mild US recession is on the horizon for early 2024 and asset quality looks set to decline from solid but unsustainable levels, with particular risks in some banks’ commercial real estate (CRE) portfolios.

We continue to expect a mild recession in early 2024, and given the funding strains on the US banking sector, there will likely be a tightening of credit conditions and rising loan losses for US banks.

Moody’s said in a statement

What This All Means

Pam and Russ Martens from Wall Street on Parade commented on these major outflows and wrote, “The speed at which the largest U.S. banks are shedding deposits is unlike anything seen in the last half century – at least. But then again, the speed at which those same banks gained deposits from the various stimulus programs during the COVID-19 pandemic was also unprecedented.”

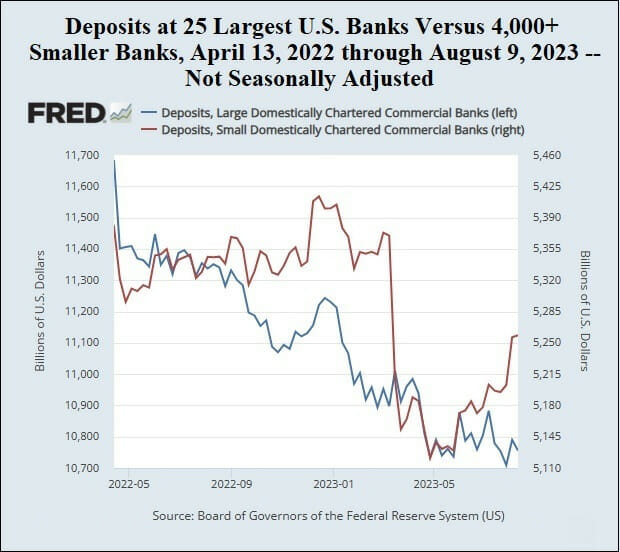

According to Federal Reserve data, for the week ending April 13, 2022, deposits at the 25 largest domestically-chartered commercial banks in the U.S. stood at $11.68 trillion (a new record) before doing a bungee dive in the following week to $11.4 trillion – likely triggered by the horrific scenes on network television of Russia’s invasion of Ukraine along with the severe economic sanctions against Russia announced on April 6, 2022 by the U.S. and other nations. This likely triggered a rush by Russian oligarchs to get their billions of dollars out of U.S. banks.

As the chart above indicates, deposits at the smaller banks also took a steep decline in the spring of 2022 but then stabilized and actually grew until the banking crisis in March of this year. Deposits at the biggest banks, however, continued their decline, consistently setting lower lows – a pattern that continues.

The Martens wrote

Moreover, because of all of this, plus with higher interest rates, banks are now increasingly denying Americans the availability of credit and lending, climbing to a 22% rejection rate, the highest in 5 years. This is a stark difference from the last years that saw banks and lenders provide deals for little to no credit. Therefore now Americans with lower credit ratings will be less likely to be approved for loans and mortgages.

But these trends are receiving very little press time. Stock market expert and analyst, and contributor for The Trends Journal, Gregory Mannarino believes that this is part of a silent revolution that Americans are finally starting to “de-bank,” and is why the media does not want to talk about it because it would trigger mass bank runs if people knew just how dire the situation was.

In a recently published piece, Mannarino wrote the following (emphasis his):

Remember this… “Nobody Knows Until Everybody Knows.” And When Everybody Knows, ITS ALREADY TOO LATE.

There is a phenomenon going on right now which is getting almost no attention from the mainstream media outlets, and for good reason. If people were made aware of what is happening right now- the entire financial system would collapse.

Here are the facts.

Right now, today, and this really got started back in early 2022, capital outflows from the major banks began to see a massive spike. In fact, as of May of this year bank deposits alone were lower by ONE TRILLION DOLLARS year over year. Moreover, this trend is worsening. Not only are bank deposits dwindling, but people are also pulling their cash out of these institutions at a record pace. It is called Un-Banking, and more people are doing it.

Un-Banking, that is people disconnecting themselves from banks by only keeping minimal deposits in the system, or pulling their cash altogether, is catching on. I am absolutely certain that moving forward more and more people are going to be Un-Banking themselves in greater and greater amounts- and that is a serious problem for the banks.

The fact is this… People have had enough! And a quiet revolution against these institutions appears to have thankfully begun!

The Bank of International Settlements, (BIS), has this to say about the current situation: “capital outflows can have a significant impact on macroeconomic outcomes.”

Today banks are seeing a virtual collapse of deposits along with cash withdrawals in record numbers. Not only are banks having to deal with lack of deposits and capital outflows, but they are also seeing loan defaults rising across the board. On a greater scale what this comes down to is a rapidly developing liquidity “crisis.”

People who are familiar with my work are keenly aware that the financial system functions in a perpetual vacuum, a constant state of illiquidity. Therefore, ever more liquidity MUST be constantly added to the system for it to function. This is the nature of the current debt-based system which is run by the collective central banking system.

What does all this mean?

Liquidity in the system is drying up FASTER as people become Un-Banked. Make no mistake, these institutions are very aware of what is going on and THEY WILL EVENTUALLY BE FORCED TO TAKE ACTION!

Limiting withdrawal amounts, or eventually stopping them altogether, is certainly a possibility. The recent actions being undertaken by central banks, raising rates, is already curtailing the availability of credit to small businesses who need access to it in order to function.

Yes. A “Quiet Revolution” has begun, and people are Un-Banking themselves…

With a situation such as this its ALWAYS better to be the first to act.

Below is a quote from the movie Margin Call.

1. Be First.

2. Be Smarter.

3. Or Cheat. (We never cheat though).

So, it’s always better to be first!

Get Un-Banked.

AUTHOR COMMENTARY

He that is surety for a stranger shall smart for it: and he that hateth suretiship is sure.

A man void of understanding striketh hands, and becometh surety in the presence of his friend.

Proverbs 11:15, 17:18

Contrary to conventional wisdom, you must be de-banked. I’ve been saying it since The WinePress was founded that you need to get your money out of the banks. These things are insolvent. Hold onto your cash and hard assets yourself. Do not leave them in a bank somewhere. Only keep the minimum there to keep the account open, pay bills, and make online purchases.

The FDIC wants people in their system for a reason so more damage and control can be inflicted.

The only thing I will say in regards to Mannarino’s article is that while some Americans are realizing what’s going on, I think these outflows of deposits are due to people being so flat broke and drowning in debt they need every penny they can get, and by keeping all that money there it costs more for them to have it there.

Also, that roller coaster ride of deposits and withdrawals makes no sense. There is, to me, some serious rigging going on there, to prop up these banks. I suspect the Federal Reserve has been secretly pumping liquidity into them.

SEE: Federal Reserve To Pump $2 Trillion Of Liquidity Into Economy To Keep The Ship Barely Afloat

The baking system is teetering on a razor’s edge, so be prepared for impact.

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

Lots of people are purchasing gold at this time; but really, with all the uncertainty out there, other than trusting God, who knows what to do. Also, a couple fast food restaurants near me is advertising no cash accepted. That’s most likely the coming trend; preparing us for a cashless society……

Even if I went pure digital (which I’ll still fight against) – I still wouldn’t go into the restaurants. It’s all gourmet food, until you know the behind the scenes.

Keeping fighting the system, I wouldn’t go to restaurants anyway, if any place refuses cash, go else ware, let them fry on their own.

I’ve been watching this & those promoting it…. some of what I see is really troubling: triumphalism & parallel society & banking….putting your money where? In whole life insurance that gains value over time through targeted investing in what? MUTUAL FUNDS. MUTUAL as in COMMON, COMMON GROUND, COMMUNISM/FASCISM.

–

They use that vehicle because its exempt from inheritance taxes & can pass on wealth (though the government goal published is to change inheritance laws by 2025), & the insurance industry has never failed. You can take out loans on the building value & use it to purchase hard assets, ‘turn deals’ and so forth, circumventing the more open & visible banking system.

–

It looks like a legitimate alternative, but is it, really? You’re still trusting banksters, and investing in any sort of mutual fund has you financing evil in the mix. They use the words ‘fearless’ and ‘transform’ a lot….and ‘branding/merchandising’ yourself & your ideas, product, service etc.

–

Most all of those involved have dropped dispensational biblical faith & fallen back toward Augustinianism & Rome’s eschatology: thinking they’re either already in Revelation 6, or that they’re going to go into the time of Jacob’s trouble & worst tribulation this world will ever see, & ‘do mighty things for God’. Big on institutionalized ‘church’. They’re hardening & readying for war, demonizing ‘negative’ and ‘jellyfish’ biblical dispensationalists who know that every dispensation ends in failure that the glory be all of God, our Lord & Saviour Jesus Christ in whom all the fullness of the Godhead dwells bodily. .

–

The ‘Christian’ parts of it emphasize Old Testament & Calvinist Augustinianism, ‘legacy’ & so forth. It’s troubling, because parts of it look so appealing, and our flesh longs for some visible hope. But, Hebrews 11-13, and James 3&4….and they make appeals to James because of ‘all the good they can do for the body & cause of Christ.’

–

Meanwhile, the openly Masonic parts of it are signaling the change of the system, too. Mannerino put up a post yesterday by a group calling themselves ‘illuminati seed’….bunch of pagan fertility cult privy member worshippers like all the rest of the antichrist crowd: and subtil. Resist it, stand your ground, and do not conform: but be REAL careful about what you champion & join yourself to.

–

1Th 4:11 And that ye study to be quiet, and to do your own business, and to work with your own hands, as we commanded you;

1Ti 2:2 For kings, and for all that are in authority; that we may lead a quiet and peaceable life in all godliness and honesty.

1Pe 3:4 But let it be the hidden man of the heart, in that which is not corruptible, even the ornament of a meek and quiet spirit, which is in the sight of God of great price.

every week my wife and I pull out all but maybe 5-$15 out of our checking account. We never have more than that in the bank